Dollar reversal After a long string of gains for the dollar, the US currency fell against all its G10 counterparts yesterday. On the other hand, it was mixed against EM currencies, as the protests in Hong Kong, polls in Brazil and heavy fighting in Ukraine hit several of the major EM markets. There may be a connection between the two sides – I suspect that the EM tensions caused investors to pare back their positioning, which nowadays would mean closing out some long USD positions. I expect the impact of these events to fade as domestic US factors come to the fore again ahead of Friday’s nonfarm payrolls and I would expect to see the dollar gradually regain the ground that it’s lost.

The Japanese data out overnight was mixed. On the one hand, retail sales picked up notably as the unemployment rate fell and cash earnings rose more than expected. On the other hand, overall household spending fell much more than expected and industrial production unexpectedly plunged. The figures suggest that domestic demand may be picking up (the household spending data is unreliable) but overseas demand remains weak. Added to the slowdown in inflation announced last Friday, today’s news in theory should increase pressure on the Bank of Japan to weaken the yen further to stimulate demand. However, recent reports say that officials aren’t too worried by the trend of slowing inflation, because they believe the main cause is falling oil prices, plus inflationary pressures are rising domestically because of a tighter labor market and higher wages – as today’s data confirm. Personally, I would emphasize the pattern in Japan’s current account surplus, which continues to fall. Until that begins to turn around, I expect the yen to remain weak.

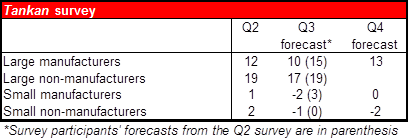

Tomorrow’s Bank of Japan tankan short-term survey of economic conditions will be a key indicator for the yen. The market expects the key large manufacturers’ diffusion index (DI) to fall to 10 from 12 in June. This is a big change from the June survey, when manufacturers forecast that it would have risen to 15 by now. In fact, expectations are that most of the major DIs will fall, reflecting the lack of a rebound from the hike in the consumption tax. Such a result could add to the speculation about further BoJ action and push the yen down.

China’s final HSBC manufacturing PMI for September was revised down to 50.2 from the provisional 50.5, but this had only a momentary impact on AUD/USD, which continued to move higher afterwards.

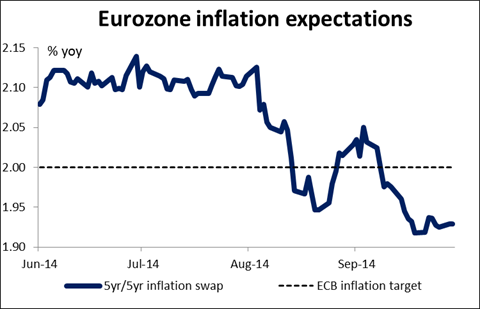

Today’s indicators: Following yesterday’s CPI data for several European countries, the Eurozone’s overall CPI for September will be released. Germany’s inflation rate (yoy basis) was unchanged while Spain’s deflation lessened slightly but Belgium slipped into deflation. Today’s Eurozone-wide figures are expected to show that the bloc’s inflation slowed slightly in September to +0.3% yoy from +0.4% in August. With only two days before the ECB meeting, data showing the risk of deflation continues in the Eurozone could add to hopes for more ECB easing, which would be EUR-negative.

German retail sales for August are forecast to rebound, while the country’s unemployment rate for September is expected to remain unchanged. Eurozone’s unemployment rate for August is also coming out along with the bloc’s CPI estimate for September.

In Norway retail sales excluding volatile items are due out.

In the UK, we get the final GDP for Q2 and Nationwide house price index for September. The former is expected to remain unchanged from the preliminary reading, while the latter is forecast to have slowed.

In the US, Conference Board consumer confidence for September is forecast to remain near its seven-year high, adding to signs of an improved US economic outlook. Chicago purchasing managers’ index for September is forecast to have decreased slightly. S & P/Case-Shiller house price index for July is also coming out.

From Canada, GDP for July is expected to have remained unchanged in pace from the previous month.

We have two speakers Tuesday: Norges Bank Governor Oeystein Olsen and Fed Governor Jerome Powell.