SYRIZA wins; now what? The left-wing SYRIZA party won the Greek election, as expected. At the time of writing, it is estimated to have 149 seats in the 300-seat Parliament, meaning that it must enter into some sort of coalition in order to have a majority. This will complicate matters, as on the one hand, all the potential coalition partners only agree with parts of the SYRIZA platform, and on the other hand, it will be hard to govern and to manage difficult debt negotiations with only a tiny majority. Not to mention that SYRIZA itself is a coalition of various factions, not all of whom agree with their leader Alexis Tsipras’ moderate views.

“There will neither be catastrophic clash nor will continued kowtowing be accepted,” Tsipras told supporters. He said the Greek people have given him “a mandate for national revival.”

As I mentioned in Friday’s comment, I think the SYRIZA victory is a good thing. I think Tsipras will encourage a long-overdue conversation in Europe about whether the current path of austerity is the best way to get Europe growing again and enable countries to repay their debts. The success of SYRIZA is also likely to encourage people in other fiscally troubled countries, such as Spain and Portugal, to vote for parties outside the mainstream. There may be some significant changes coming to European economic policy. We will know more later today, when the regular Ecofin meeting will probably discuss what to do about Greece. Dutch Finance Minister Jeroen Dijsselbloem, who chairs the meetings, has said that while there is “room to manoeuvre” with Greece over its adjustment program, there’s little support within the group for a haircut on Greek debt.

What are the risks? The problem is, some of what Tsipras wants is contradictory. He intends to ask the Eurozone to extend Greece’s debt and agree to a more expansive fiscal policy. It’s questionable whether they will extend the debt, and if they do, why should they simultaneously allow a more expansive fiscal policy? He plans on squaring this circle by improving tax collection, although that has never been possible before. We’ll see if he can do it any better. In any event, the first problem will be to prevent capital flight out of Greece and to secure within 10 days an extension of the ECB’s emergency liquidity assistance, which is what’s keeping the Greek banking system afloat. Without that, the banking system will quickly grind to a halt. He also has to improve tax collection, as many citizens apparently stopped paying some of their taxes on the assumption that taxes that SYRIZA has opposed in the past would no longer have to be paid. This is crucial because if taxes don’t meet their target, the IMF may not certify that Greece is meeting its obligations with regards to the final EUR 7.2bn tranche of the support program. Without that money, Greece would have serious problems. I think the odds are that, initially at least, the headlines suggest more confrontation and are therefore negative for the euro. Later as reality sinks in, the two sides are likely to strike a deal that keeps Greece in the euro and keeps pressure on the country, with perhaps some face-saving concessions to allow Tsipras to accept the terms.

More on QE: The euro came under some pressure on Friday after Benoit Coeure, the ECB’s head of market operations, said “If we haven’t achieved what we want to achieve, then we’ll have to do more, or we have to do it for longer.” Italian Central Bank Gov. Ignazio Visco also said that “we are open-ended” about asset purchase. This was only confirming what ECB President Draghi implied at his press conference: that if inflation hasn’t gone back to around 2% by the time the QE purchases are scheduled to end in Sept. 2016, they will have to extend them. Nonetheless, this was the first hint that they might increase the amount of purchases as well as lengthen the time. Of course this is a 2016 event we are talking about, but as we’ve seen with the Bank of Japan, there can be surprises. EUR-negative.

Japan’s trade deficit for December narrowed more than expected on stronger-than-expected exports. This could be the first sign that the weaker yen is finally feeding through to increased exports. Yet the yen weakened immediately following the report, perhaps because the minutes of the Dec. 18-19 Bank of Japan meeting, released at the same time, showed continued determination to keep loosening until they hit their 2% inflation target.

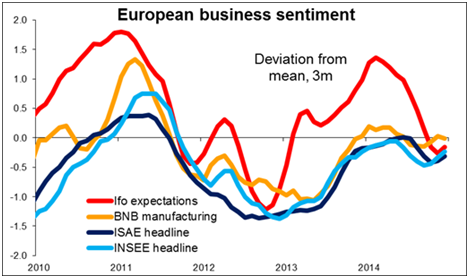

Today’s highlights: During the European day, we get the German IFO survey for January. All three indices are expected to have risen as falling oil prices boost sentiment. This comes on top of the strong ZEW survey released last Wednesday, yet it will probably not be enough to reverse the negative sentiment towards EUR. For example, Friday’s better-than-expected PMIs for the Eurozone did nothing to halt the currency’s decline.

Rest of the week: As for the rest of the week, the highlight will be the FOMC meeting on Wednesday. The minutes of the previous meeting showed that the Fed isn’t concerned about the stronger dollar and was concerned about the tight labor market, showing that it remained on track to hike rates. However, the weakness in the European and Canadian economies could prompt Fed officials to reassess their outlook for the US economy and push back expectations for a rate hike. There is no press conference scheduled after the meeting.

On Tuesday, the 1st estimate of UK Q4 GDP is expected to show a rise in the pace of growth from Q3. Given the weak industrial production data in October and November, we wouldn’t be surprised with a below consensus growth rate. Along with the falling inflation rate, this is likely to keep the markets convinced that the first rate hike won’t be until after the general election in May, keeping GBP/USD under pressure. In the US, we get durable goods for December.

On Wednesday, besides the FOMC meeting, the Reserve Bank of New Zealand meets. At its December meeting, the Bank stated that the next move in rates was likely to be up. However, following the sharp fall in inflation in Q4, below the lower boundary of the Bank’s range target of 1%-3%, they may change their stance and return to neutral again. In Australia, the Q4 CPI is anticipated to ease in pace. The market seems to give more attention to the trimmed mean CPI, which is also expected to decelerate a bit. The threat of plunging inflation, dragged down mainly by the low oil prices, increase the likelihood for the RBA to cut rates in its February meeting. This could put further downward pressure on AUD.

On Thursday, we get the German CPI for January, starting with several Lander releasing their data in the course of the morning. As usual, we would look to the larger states for guidance on where the headline figure will come at. Overall, the forecast is for the national CPI to fall to deflation, which could prove EUR-negative.

Finally on Friday, Eurozone’s preliminary CPI for January is expected to fall at an accelerating pace, suggesting that the deflationary pressures have increased in the region. In the US, the 1st estimate of GDP for Q4 is expected to show that the US economy expanded at a slower pace than in Q3. The 1st estimate of the core personal consumption index, the Fed’s favorite inflation measure, is forecast to have eased from the Q3.