Dollar falls into Jackson Hole After several days of across-the-board gains, the dollar fell across the board yesterday. It was lower against all the G10 currencies and among the EM currencies we track, gained only against BLR and CNH. The weakness of the dollar was not justified by the economics, which were uniformly supportive: existing home sales, the Markit US manufacturing PMI, leading index and Philadelphia Fed business outlook were all higher than expected and higher than the previous month, while jobless claims were lower. The dollar’s weakness was therefore probably due to investors’ anticipation of dovish comments at today’s Jackson Hole economic conference (see below). In that respect, I think it will only be temporary and offers good opportunities for setting up long USD positions.

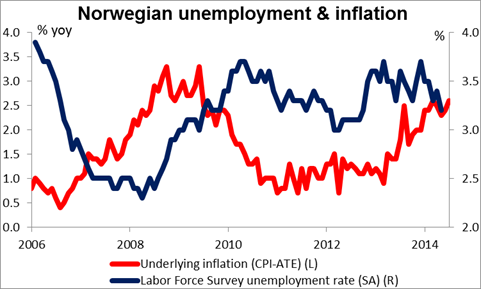

The best performing currency over the last 24 hours was the NOK, which soared yesterday after it was announced that the mainland economy expanded 1.2% qoq in Q2, more than double the 0.5% pace of Q1 and far exceeding estimates. It has managed to maintain the gains into today. The report only confirms the other recent solid news from Norway, including both one of the lowest unemployment rates and highest inflation rates in Europe. The next Monetary Policy Report, due out on Sep. 18th, should therefore have a fairly hawkish view (for Europe, at least) which is likely to keep the currency underpinned for now. I expect USD/NOK to test the 6.1300 zone, which is the 38.2% retracement of the 8th May- 6th August longer-term uptrend. A clear dip below 6.1300 would most likely trigger further extensions towards the key support of 6.1000.

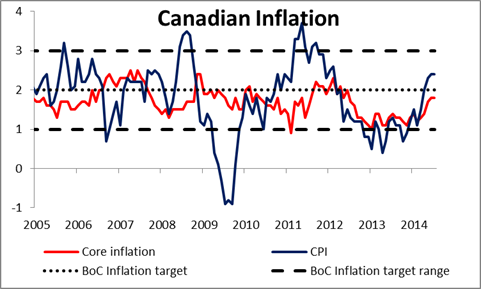

Today’s events: Friday’s calendar is very light. We have no major indicators coming out from Asia, Europe, the UK or the US, only Canada. The country’s CPI is forecast to slow to 2.2% yoy in July, from +2.4% yoy in the previous month and retail sales for June are expected to decelerate on a mom basis. CAD-negative

The most important event on Friday will be Fed Chair Janet Yellen’s keynote speech at Jackson Hole economic symposium. The theme this year is “Re-evaluating Labor Market Dynamics” and Yellen’s speech is simply titled “Labor Markets”. After Wednesday’s FOMC minutes, which revealed growing pressure from the hawks to begin hiking rates, investors’ attention will be focused on any possible change from her previous balanced comments regarding employment conditions, which emphasized both the progress made in reducing the unemployment rate and the contradictory message sent by other employment indicators, such as the large number of the long-term unemployed and sluggish wage growth (problems now summed up by the FOMC as “underutilization of labor resources”). However, I would not expect her to come out with much of a change in tone. Fed Chairs have used the Jackson Hole seminar in the past to send signals to the market, most recently in 2012, when Bernanke hinted that another round of quantitative easing was possible, as indeed happened a few weeks later. But the FOMC has been moving away from a “superstar” system and more towards a committee approach to making policy. In that respect, for the Chair to announce a major change in policy now – a few days ahead of an employment report (Sep. 5) and a couple of weeks ahead of an FOMC meeting (Sep. 16-17) might be considered “front running” the Committee. Having said that, the market is prepared for a neutral to dovish speech from Yellen, so such comments would probably not be market-affecting. The risk is that she says something more hawkish and takes the market by surprise.

ECB President Draghi will also be speaking at the seminar. With Europe’s unemployment rate stubbornly high, it will be interesting to hear what advice he has. The ECB has not released a title for his speech, which will be given over lunch.