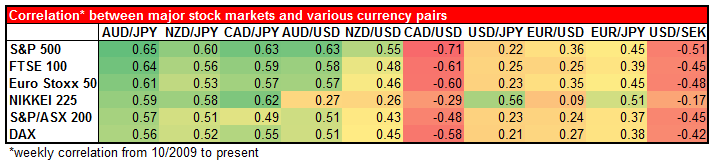

Yen gaining on risk aversion The dollar was opening little changed in Europe from its levels Friday morning. The only noticeable trend within the G10 was a strengthening yen. This stands to reason, as stock markets around the world – including Japan – fall. USD/JPY is strongly positively correlated with Japanese stocks (USD/JPY has a.56 correlation with Nikkei over the last five years, while EUR/JPY has a .45 correlation with S & P 500), so it’s normal behavior for the yen to strengthen when the stock markets fall. A quick search turned up only a handful of tiny stock markets that rose on Friday – Peru, Jamaica, Ukraine, Serbia, Latvia, etc. In Asia today, only Pakistan.

It seems to me that attempts by US officials to reassure the markets are backfiring. Over the weekend, Fed Vice Chair Stanley Fischer said that if foreign growth is weaker than anticipated, the Fed might “remove accommodation more slowly than otherwise.” Other officials echoed his concern about the impact that weak growth elsewhere, particularly in Europe, might have on the US. While perhaps his comments and others were meant to reassure the markets that the Fed was not oblivious to these concerns and would not raise rates too quickly, the comments seem to be undermining confidence in the US recovery. With the S & P 500 sitting just on top of its 200-day moving average (1905.22, vs Friday’s close of 1906.13), stock markets – and the yen – are looking finely balanced. (Although to be fair, the last two times the S & P 500 broke through the 200-day moving average from the top in June and Nov. 2012, there was no dramatic further decline.)

I would recommend caution for those investors who are using JPY as a funding currency. On the other hand, the equities that usually suffer most when currencies decline are the commodity currencies (AUD, NZD, CAD) and SEK. Short AUD/JPY might be one way to express a negative view on global equities through currencies, although given the risk of a surprise in the Chinese indicators coming out this week (see below), CAD/JPY might be a better bet. CAD/JPY is strongly correlated with US stocks (0.63)

China announced a huge reduction in its trade surplus in September from August’s record levels. Exports rose more than expected, while imports soared. This is good news for everyone. The strong exports will support growth in China, while strong imports and a reduced trade surplus mean the benefits of that growth are being distributed both among China’s trading partners and within China (that is, households are benefitting more as well). AUD and NZD were both rising vs USD into the figure and continued to gain afterwards, although AUD/USD remains below Friday’s opening level, perhaps because of the impact of lower global stock markets.

China will issue some of the most important releases this week, including money and bank lending growth, consumer and producer prices, foreign direct investment, and business sentiment. The market will want to see if the problems in the property market have depressed activity further. In that respect, the bank lending figures will be closely watched.

Today’s activity likely to be light: Today may be relatively quiet as Japan was on holiday in the morning (Sports Day) and in the afternoon both the US (Columbus Day) and Canada (Thanksgiving) are on holiday, although the markets are still open in the US. As for indicators, there are no major indicators coming out from the Eurozone, the UK nor the US. There are three speakers: ECB Executive Board member Peter Praet Bundesbank President Jens Weidmann in Europe and Chicago Fed President Charles Evans. Weidmann will speak on “Conditions for a Stable Currency Union;” it will be interesting to hear how his vision on this matter differs from ECB President Draghi’s. The two have expressed quite different views on what needs to be done to keep the Eurozone together.

Rest of the week: There are no major central bank policy meetings scheduled for this week. There will be however the usual round of speakers, including Fed Chair Janet Yellen herself (Friday) and several of her FOMC colleagues, including Messrs. Bullard, Lockhart, Plosser, Evans, Tarullo and Kocherlakota. ECB President Draghi will give an introductory speech at an ECB conference on Wednesday and RBA Deputy Gov. Debelle speaks Tuesday at an investment conference.

As for the indicators, on Tuesday, we get UK’s CPI for September and the forecast is for the inflation rate to ease again. On top of the recent poor data, this will most likely push expectations for BoE tightening further back, probably after the country’s general elections in May. From Germany we get the ZEW survey for October. The current and the expectations situation are expected to decline, reflecting the concerns about the nation possibly falling into recession. Eurozone industrial production for August is anticipated to drop in line with the fall in bloc’s strongest economies.

On Wednesday, the highlight will be the UK unemployment rate and average weekly earnings, both for August. The consensus is for the unemployment rate to decline, while the average weekly earnings are projected to accelerate. That could boost GBP. In the US, we get retail sales for September. Both the headline figure and sales excluding the volatile items of autos and gasoline are forecast to decelerate. The Fed releases the Beige book.

From Canada, building permits plunged in August, while housing starts rose modestly in September. The market will be waiting to see the existing home sales for September to have a clearer view of the nation’s housing market activity. ECB President Mario Draghi will speak twice on Wednesday in Frankfurt, and he may repeat his pledge that the ECB is “ready to alter the size and/or the composition of our unconventional interventions” but this time to a different audience.

On Thursday, we get the Eurozone’s final CPI for September and from Canada, manufacturing sales for August. We have several Fed speakers scheduled as well.

Finally on Friday, the spotlight will be on Fed Chair Janet Yellen’s keynote speech at a Boston Fed conference on “Inequality of Economic Opportunity.” As for the indicators, from the US we get building permits and housing starts both for August. In Canada, CPI for September is due out.