EUR/USD salutes the new year by mimicking it EUR/USD saluted the New Year 2015 by mimicking it – hitting 1.2015 (and even a bit lower) and then gapping lower at the opening Monday. ECB President Draghi was quoted in the German paper Handelsblatt Friday as saying that the risk that the ECB doesn’t fulfill its mandate of price stability is higher than it was six months ago and that they are “in technical preparations” to institute quantitative easing early in 2015 if necessary. The first part of his statement is obviously true; all you have to do is wait for this Wednesday, when the Eurozone CPI for December is forecast to go into deflation (-0.1%) as opposed to +0.5% back in June. Even that figure was well below their 2% target, though. The second part though depends on getting agreement on the ECB board. As mentioned on Friday, not everyone on the board agrees (even though Draghi said the Board was “unanimous”) and furthermore, the Greek elections may prove a legal obstacle to instituting QE in January and perhaps later as well.

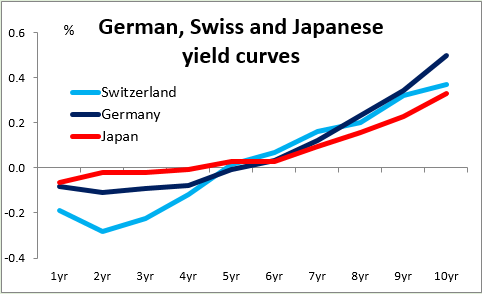

Draghi’s comments not only pushed EUR/USD down to right above the psychological line of 1.2000, but also pushed Eurozone bond yields, already at record lows, down further. German Bund yields for example are now negative out to 5 years and 10-year yields went below 50 bps for the first time. There’s now not so much difference overall between German yields and Japanese yields. Does this presage Japanese-style deflation and therefore Japanese-style monetary policy in the Eurozone? It might, eventually. In any case, if they do not institute QE, then there is likely to be a big sell-off in Eurozone bonds and repatriation of currency that would push EUR/USD even lower.

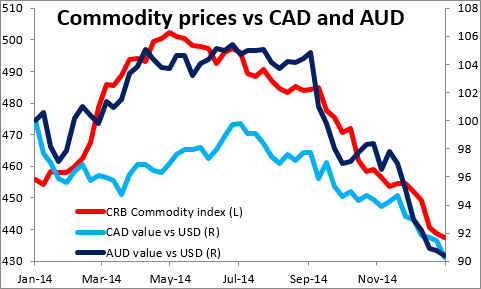

Commodities were pushed lower by the strong dollar as well, and with them the commodity currencies fell. USD/CAD hit a new high for this cycle. Lower commodity prices resulting from Draghi’s warning about the risks of low inflation seems like a self-fulfilling prophecy, even more so as the US 5yr/5yr forward inflation swap fell further. His concern that inflation expectations are becoming unanchored seems to be one of the reasons why inflation expectations are becoming unanchored. As inflation expectations fell, so too did expectations for the Fed funds rate, despite comments from Cleveland Fed President Loretta Mester that she “could imagine interest rates going up in the first half of the year.”

In fact the dollar gained against all the G10 currencies and most of the EM currencies that we track. The US currency regained parity vs CHF as the Swiss National Bank was apparently forced to intervene to defend the EUR/CHF floor. Swiss bond yields are now negative out to four years and the 10-year yield is about the same as in Japan.

One indication of where the currency markets may be headed this year: despite all the talk about the erosion of the dollar’s standing in the world financial system, the IMF Friday announced that the US currency’s share of global foreign exchange reserves rose to 62.3% in Q3 last year from 60.7% in Q2. This was the highest level since Q4 2011. The euro’s share on the other hand fell to 22.6% from 24.1%, its lowest level in over a decade. That means central banks chose not to rebalance their falling reserves as the euro fell during the quarter. These folks are the closest there are to having inside information in the FX market so we should take their views seriously. Talk of the dollar’s demise is premature.

Today’s highlights: On Monday, the main release will be the German preliminary CPI for December. As usual, several of the lander release their data before the national figure and the market looks at the larger ones for guidance. The consensus is for a fall in the national yoy rate to +0.2% from +0.5%, which could prove EUR-negative.

In the UK, the construction PMI is forecast is estimated to have declined in December.

As for the speakers, Minneapolis Fed President Kocherlakota spoke in Boston on Sunday and argued against requiring the Fed to use a mathematical rule to set policy. Republicans are considering introducing rules that would limit the Fed’s independence and room for discretion in setting monetary policy. Also Boston Fed President Rosengren released the text of a speech he will make later in the day in which he said low core inflation and wage growth “provide ample justification for patience,” but he doesn’t vote this year so what does it matter? During the European day, San Francisco Fed President John Williams participates at a panel on “Housing, Unemployment, and Monetary Policy”. Norges Bank Governor Oeystein Olsen and Swiss National Bank President Thomas Jordan will also speak.

Rest of the week: Tuesday we get the final PMIs for December. In the US, the ISM non-manufacturing index is forecast to have declined, following the disappointing manufacturing ISM on Friday. The US factory orders for November are also coming out.

On Wednesday, besides Eurozone’s CPI data, the Fed releases the minutes from its latest policy meeting, when officials dropped the “considerable period” phrase and instead said the Committee “can be patient in beginning to normalize the stance of monetary policy.” The market is likely to look into the minutes for more insights regarding the meaning of the new phrase. The ADP employment for December is also coming out two days ahead of the NFP release and is expected to show a faster rate of growth in jobs.

On Thursday, the Bank of England Monetary Policy Committee meets. It’s unlikely to change policy and therefore the impact on the market should be minimal as usual. The minutes of the meeting however should make interesting reading when they are released on 21st of January. Eurozone’s PPI and retail sales both for November are also coming out.

Finally, on Friday, the major event will be the US non-farm payrolls for December. The market consensus is for an increase in payrolls of 240k, down from the stunning print of 321k in November but still strong. That would show that the economy has added at least 200k jobs for 11 consecutive months and could result the biggest annual gain in employment since 1999. The unemployment rate is forecast to have declined to 5.7% from 5.8%, while average hourly earnings are expected to accelerate on a yoy basis. Such a strong employment report could push Fed funds rate expectations up and therefore support the dollar. Canada’s unemployment rate for December is also coming out.