Dollar generally higher despite lower US rates The dollar was opening higher in Europe against almost all the G10 currencies and the EM currencies that we track even though Fed funds rate expectations ended the day lower Friday and bond yields declined somewhat. Fed Chair Janet Yellen Friday said “conditions may warrant an increase in the federal funds rate target sometime this year” but that rates would rise “only gradually” and that tightening could even reverse if conditions warranted it. These comments were quite in line with what Fed officials have been saying up to now. Judging from the market response though, the statements increased the market’s conviction that a rate hike is coming (hence the stronger dollar) while lowering the market’s assumed path of rate increases (hence lower interest rates).

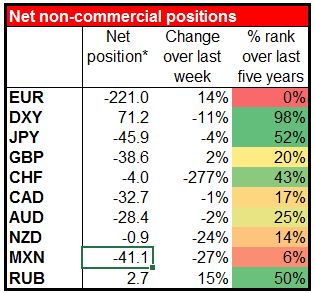

The Commitment of Traders (COT) report showed that while investors generally became less bullish on USD, reducing long DXY positions and closing out some short currency positions, they increased their net short EUR positions by a substantial 14% to a record short position. This suggests that in addition to USD strength, we are likely to see EUR underperformance in the coming week. Quantitative easing plus Greece’s troubles are probably behind that.

Greece the focus of attention again Attention today is likely to focus on Greece as PM Tsipras updates Parliament on talks held over the weekend between the Greek government and the group of creditors formerly known as the troika (European Commission, ECB and the IMF). The Greek government apparently has submitted the long-awaited list of reforms to the lenders. According to the FT, officials who have seen the list said that while it contained some concessions, it depended too much on optimistic economic assumptions and suffered from the same lack of detail in some of the areas that have caused concerns during previous talks. In particular, the list failed to include reforms to labor laws and Greece’s pension system, two areas that monitors have insisted are essential to finalising the bailout program but that Greek officials say remain “red lines.” So there still remains a big gap between the two sides.

According to the Greek newspaper Kathimerini, even if there is a broad agreement between Greece and its creditors, it is unlikely that eurozone finance ministers will meet this week or even the week after to approve the release of even part of the EUR 7.2bn remaining in bailout money. Part of the reason is because of the Easter Sunday holiday, which falls this coming Sunday according to the Western calendar and the following Sunday according to the Greek Orthodox calendar. But also it appears that the technocrats have made only “limited progress,” the newspaper said.

The problem is, just how much longer does Greece have? How much more money does it have and how long can it finance itself for? Some reports have said that it will run out of money by April 8th. If so, and they still haven’t worked out their differences by now, then we could be in for some last-minute tensions.

Oil plunges on possible Iran settlement Oil plunged Friday as diplomats worked towards a settlement of the Iranian nuclear issue. Settling that problem would free about 1mn b/d supply to come onto the world market, worsening the glut on the market. It may be that market participants expect Iran to co-operate in order to achieve an agreement, which not only would free Iranian oil for the market but also reduces the risk of a supply interruption from Saudi’s incursion into Yemen. I remain bearish on oil because of the increase in US supply, as I mentioned Friday, regardless of what happens with Iran. This would suggest long USD/CAD and USD/NOK positions could be profitable.

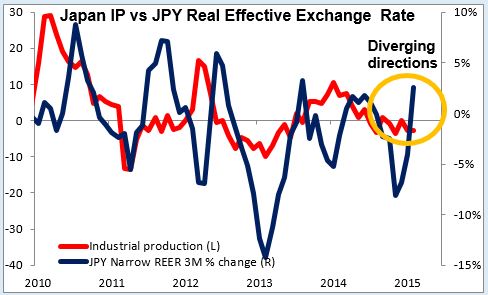

Japan industrial production fell in Feb Industrial production fell 3.4% mom, a larger decline than expected. Some of the decline could be due to the Chinese New Year in February. Nonetheless, the news highlights the fragility of Japan’s recovery and is likely reaffirm the administration’s commitment to a weaker currency to encourage exports. JPY-negative.

Today’s highlights: During the European day, German CPI for March is coming out, after several regional states release their data in the course of the morning. As usual, we will look at the larger regions for a guidance on where the headline figure may come in, as an indication for the near-term bias of the common currency. A better-than-expected headline figure could support EUR a bit.

The Swiss National Bank releases its weekly sight deposit data, which could show if the Bank intervened in the FX market in the week ended March 27. Indications of intervention could weaken CHF somewhat. So far the SNB does not seem to have intervened; on the contrary, deposits have decreased a bit. However, EUR/CHF has started to move down again recently and so it will be worth noting whether they have resisted the move.

In the UK, we get mortgage approvals for February.

In the US, we get the personal income and personal spending for February. Personal income is expected to rise at the same pace as previously, while personal spending is anticipated to rise, a turnaround from the previous month. The nation’s yoy rate of the PCE deflator and core PCE are also coming out. The nation’s yoy rate of the PCE deflator is expected to rise a bit, while the core PCE rate is forecast to remain unchanged, in line with the 3rd estimate of Q4 core PCE in Friday’s GDP figures. Pending home sales for February and Dallas Fed manufacturing index for March are also coming out.

Rest of the week: On Tuesday, in the UK, the 3rd estimate of Q4 GDP is coming out. The final estimate of GDP figure is expected to confirm the preliminary reading. Therefore the market reaction could be minimal as usual. The 1st estimate of Eurozone CPI for March is also coming out. Following the introduction of the quantitative easing program by the ECB to boost growth and prices, the impact of the CPI on EUR is not as great as it used to. Daniele Nouy, Chair of the Single Supervisory Mechanism, will testify to the European Parliament. She may give some indication of how her department is getting along with the ECB Governing Council as they strive to regulate Greek banks while keeping the country from defaulting.

On Wednesday, during the Asian session, Bank of Japan releases its Tankan business confidence survey for Q1. All the indices for larger companies and the small companies are forecast to increase. This would be a favorable result for Japanese stocks and USD/JPY could rise as a result.

The manufacturing PMI figures for March from several European countries, the UK and the final figure for the Eurozone as a whole are also due out. As usual, the final forecasts for the French, the German and Eurozone’s figures are the same as the initial estimates. In the US, the main event will be the ADP employment report released as usual two days ahead of the NFP. The ADP report is expected to show that the number of new jobs in March increased from February, which would be USD-supportive. The ISM manufacturing PMI is also due out.

On Thursday, the only noteworthy indicator we get is the UK construction PMI for March. The minutes from the March ECB meeting will be released, which will shed some light on members’ views on QE.

Friday is NFP day! The market consensus is for an increase in payrolls of 250k in March, down from 295k in February. The expected increase in March seems moderate compared to the astounding increases in the recent months. Nonetheless it would still be a strong figure consistent with a firming labor market. The unemployment rate is forecast to remain unchanged at 5.5%, while the average hourly earnings are expected to accelerate a bit on a yoy basis. A robust labor report in line with estimates would keep the Fed on track to raise rates this year, which could help USD recover its lost glamour. Elsewhere in the world, Good Friday will be a national holiday in Europe, Australia, New Zealand and Canada.