FOMC stands pat, RBNZ more dovish The Fed and RBNZ were both largely as we expected: the FOMC statement was largely unchanged while the RBNZ changed from a tightening bias to strictly neutral. As a result, the dollar rose against almost all the currencies we follow (JPY being the main exception), while the NZD was the biggest loser.

The FOMC statement was little changed from last time. The most important change was that it referred to “strong job gains” instead of “solid job gains,” meaning that the Committee is a bit more confident about the employment picture, and said the economy is expanding at a “solid pace” instead of a “moderate pace,” meaning they are more confident about the economy overall. They said that inflation is now running below target “largely” because of low oil prices (instead of “partly”) and added the phrase “inflation is anticipated to decline further in the near term,” but continued to say that they expect it to return to their 2% target. Perhaps most importantly, they qualified that prediction by saying inflation would return to 2% “over the medium term,” which sounds like they are pushing it out further into the future than before. In other words, they attribute the below-target inflation rate to the fall in oil prices but are looking through that, perhaps because “recent declines in energy prices have boosted household purchasing power” (another new line). They still expect inflation to come back to target, although they realize it may take longer than they had thought. As for the rest of the world, the only reference they made was to add “international developments” to the end of the long list of things they would be looking at as they assess the information that they’ll be monitoring.

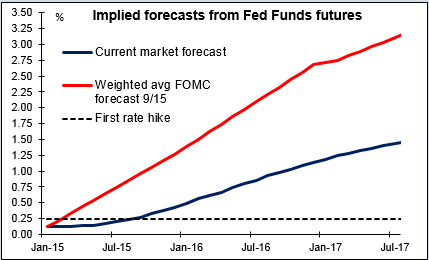

The market view of the statement was mixed Fed funds rate expectations crashed – the expected Fed funds rate for Dec. 2017 was down a tremendous 11.5 bps. Ten-year yields were also down 10 bps. This may be because of the addition of the “over the medium term” phrase. On the other hand the dollar rose and stock prices fell because they did not retreat from their tightening bias – they are still on track to hike rates later this year, even if the market now thinks that the pace of tightening will be slower than previously expected. I remain a total USD-bull. The FOMC is clearly determined to begin the process of normalizing rates, which sets it apart from virtually all other central banks, and this should keep the USD underpinned.

The RBNZ on the other hand followed the global trend towards loosening In the Dec. 11th statement, Gov. Wheeler said that “Some further increase in the OCR (official cash rate) is expected to be required at a later stage.” This time however he said ”In the current circumstances, we expect to keep the OCR on hold for some time.” On top of which, he added that “Future interest rate adjustments, either up or down…” will depend on the data. So they went from a tightening bias to a neutral bias and even held out the possibility that the next move in rates would be a cut. The statement was focused on the downside risks to growth. Wheeler also continued to complain about the overvaluation of the NZD, a veritable tradition at the RBNZ:

- While the New Zealand dollar has eased recently, we believe the exchange rate remains unjustified in terms of current economic conditions, particularly export prices, and unsustainable in terms of New Zealand’s long-term economic fundamentals. We expect to see a further significant depreciation.

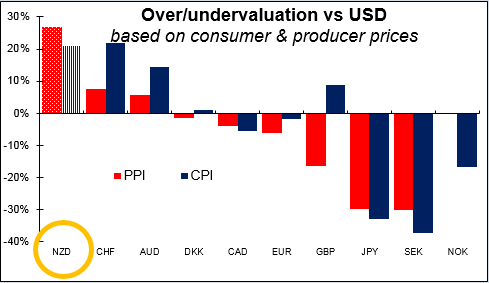

He does have a point; according to Bloomberg’s PPP calculations, the NZD is about as overvalued as the CHF, the most overvalued currency, based on consumer prices and is far and away the most overvalued currency in the world based on producer prices, although the OECD methodology puts it only about 7% overvalued vs USD. Nonetheless, I still expect the NZD to do better than AUD. We’ll have to see whether the Reserve Bank of Australia also changes its bias at next week’s meeting. Currently, their policy is strictly neutral: they expect “a period of stability in interest rates.” After the various surprise loosening moves, from Denmark to Singapore and now New Zealand, I wouldn’t be surprised if Australia shifted too. In fact, the market is now likely to expect most central banks that don’t already have a loosening bias to shift.

Keep watching Greece The Greek situation has not settled down; on the contrary, it seems to be getting more and more agitated. Greek stocks were down another 9% or so yesterday while 3-year bond yields moved up 275 bps to 16.73%. Feb. 5th is the next pressure point, when the country’s emergency liquidity assistance (ELA), the ECB lifeline that keeps Greece’s banks afloat, is up for renewal at the same time as the Parliament reconvenes. The Greek situation still has the potential to roil the EUR more.

Today’s highlights: During the European day, the main release will be the German preliminary CPI for January. Before the headline figure is released, several regional states will release their January data. As usual we would look at the larger states for guidance on where the headline reading is going to come in at. The consensus is a decline to deflation, which could add further downward pressure on the Eurozone’s estimate CPI to be released on Friday. Overall, the forecast to fall to deflation, could prove EUR-negative. German unemployment rate for January is expected to remain unchanged from December.

Eurozone’s M3 money supply is forecast to have risen 3.5% yoy in December, a slight acceleration from 3.1% yoy in November. This will push the 3-month moving average to accelerate if the forecast is met. The bloc’s final consumer confidence for January is expected to remain unchanged from the preliminary print.

Sweden’s economic tendency survey for January is expected to increase marginally from the previous month.

In the US, we get the initial jobless claims for the week ended Jan.24. Pending home sales for December is forecast to decelerate. This is in line with the moderate increase in existing home sales in December.

In New Zealand, we get building permits for December.

We have no speakers on Thursday’s agenda.