US indicators disappoint again As I mentioned on Friday, investors are concerned that global growth – including the US – is slowing. The dollar bulls had hoped that the March US durable goods figure would disprove this theory, but in the event the figure was just as disappointing as the other recent US data. The headline figure rose nicely on aircraft and auto orders, but core orders (nondefense capital goods orders excluding transportation) were down once again. Many Wall Street economists downgraded their Q1 GDP forecasts based on the number. The Atlanta Fed’s GDPNow forecasting model for example was revised down 10 bps to +0.1%. The weaker GDP forecasts are likely to weigh on the dollar this week, particularly if today’s Dallas Fed index disappoints (see below). It seems the only rosy spot on the economic map is Europe, where the Ifo business climate index rose in April, suggesting the weak April PMI might have been a fluke.

Eurogroup meeting shows no progress with Greece Eurozone finance ministers met Friday and discussed Greece. How did the meeting go? Let’s ask Malta’s Finance Minister Edward Scicluna. He told Bloomberg, “I would describe today’s meeting as complete breakdown of communication with Greece.” As for the future, Eurogroup chairman Dijsselbloem noted “I don’t dare say whether there will be some kind of result” on Greece at the next Eurogroup meeting on May 11. “It seems too quick for me given the current situation. It can be achieved, but it’s starting to become theoretical.” Asked if there were a “plan B” for Greece if they couldn’t meet the lenders’ demands, German Finance Minister Schäuble said simply, "You shouldn't ask responsible politicians about alternatives," because of course they can never confirm them.

ECB President Draghi said the ECB would continue to supply emergency liquidity to Greek banks as long as the banks were solvent, but that they would discuss the size of the “haircut” on Greek collateral at the next Governing Council meeting on 6 May. It seems that the ECB may once again be put in the position of taking actions that the elected politicians can’t. They could simply declare that the Greek banks are insolvent and stop supplying ELA to them, which would effectively shut down the Greek banking system. This would be similar to what happened in Cyprus. Another possibility, which is beginning to look more likely, is that they start raising the haircut on collateral, which would limit the amount of ELA that Greece could get. That would also force a response from the Greek government, probably including capital controls, but it would make it easier to restart the financial system than if the banks are declared insolvent.

Don’t forget, what these discussions are about is just whether to give Athens the remaining €7.2bn of bailout funds that it’s owed under the terms of the previous agreements. That would not be enough to set the country on a sustainable path, because as Finance Minister Varoufakis frequently reminds us, there is no way the country can repay its debts while it’s in recession.

Iron ore price recovering The price of Australia’s iron ore exported to China has risen 17% since hitting bottom on April 10th. That’s probably one reason AUD has been doing a bit better recently, although the currency certainly hasn’t risen by 17%.

Today’s highlights: Today is a relatively light day. There were no major indicators release during Asian time and there are no major releases scheduled from Europe.

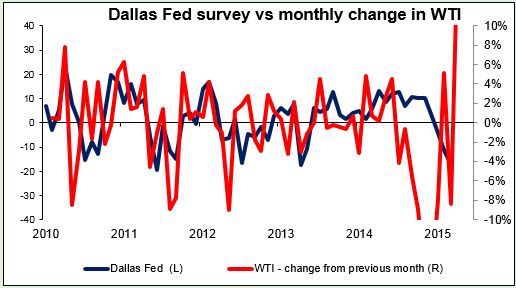

In the US, the only noteworthy indicators we get are the US preliminary Markit service sector PMI and Dallas Fed manufacturing index both for April. The Dallas Fed index is expected to rise. Given the region’s dependence on the oil industry, that would be quite an achievement. The index has already fallen for six months in a row. However, the recent rebound in oil prices suggests that it is indeed possible.

As for the speakers, ECB Vice President Vitor Constancio and ECB Executive board member Benoit Coeure speak. Norway central bank Governor Oeystein Olsen also speaks.

As for the rest of the week, many central banks hold their policy meetings. The spotlight will be on Wednesday when the Federal Open Market Committee (FOMC) meets. With no press conference scheduled or new forecasts at Wednesday’s meeting, the focus will be on the accompanying statement for any hint for the timing of the first rate hike. As mentioned in previous statements, an increase in the target range for the fed funds rate remains unlikely at April’s meeting. Therefore, no substantial change in the statement is expected at this meeting and the Committee may simply repeat that economic growth has moderated somewhat and that they continue to assess progress toward maximum employment and price stability. Other central bank meetings include Sweden’s Riksbank, also on Wednesday, and Bank of Japan (BoJ) and Reserve Bank of New Zealand (RBNZ) on Thursday. Sweden has said it remains in easing mode, and a majority of analysts expect a cut; estimates range from –0.35% to -0.5% (current rate: -0.25%). The BoJ is not likely to make any changes, but this week’s meeting brings new long-term forecasts in the semi-annual outlook report. If the report forecasts that it will take longer to return to 2% inflation, the Committee could use that as the trigger for an increase in stimulus, which would probably be JPY-negative. As for the RBNZ, although they recently signaled a shift towards an easing bias, the market expects no change at this week’s meeting and neither do we.

Other major indicators: On Tuesday, the UK 1st estimate of Q1 GDP is coming out. The forecast is for the growth rate to decelerate a bit despite the strong industrial production in January and February. On Wednesday, German CPI for March is coming out. Following the introduction of the quantitative easing program by the ECB, the inflation figures are not as market-affecting as before. In the US, the 1st estimate of Q1 GDP is expected to show that the US economy expanded at 1.0% qoq SAAR, a slower pace than 2.2% qoq in Q4 2014, according to the Bloomberg survey. However, as mentioned above many economists trimmed their forecasts so the published consensus figures may not reflect the most up-to-date thinking. The 1st estimate of the core personal consumption index, the Fed’s favorite inflation measure is also coming out. A weak reading could prove USD-negative. On Friday, during the Asian day, we have the usual end-of-month data dump from Japan, including the National CPI rate for March and the Tokyo CPI rate for April. The market reaction on these releases could be minimal as usual.