Employment situation continues to improve Yesterday’s jobless claims were better than expected at 268k – the news reports say they were the second-lowest in 15 years. In fact they’re even better than that, because 15 years ago, there were 36.7mn fewer people living in the US and 14.3mn fewer people working. If we adjust for the change in the labor force, the initial jobless claims are the lowest on record (= back to 1967). Continuing claims are not quite there yet, but almost.

Nonetheless, the dollar weakened as traders braced themselves for a possible nonfarm payroll figure of less than 200k. Remember that the March NFP survey was taken on the week of March 14th, whereas yesterday’s figures refer to the week of March 28th, two weeks later. Jobless claims the week of the 14th were higher (293k), perhaps as a result of bad weather, which may be more relevant for today’s NFP figure. The market consensus from analysts for the NFP is 245k (see below), but many investors see the risk on the downside owing to mean reversion after a string of exceptionally strong numbers (average for the last four months is 322k). The last below-200k number was in August last year, but that got revised up to 213k. The last final number below 200k was in February 2014. Nonetheless, US bond yields moved higher as the good figure encouraged some profit-taking on bonds.

Don’t place too much importance on today’s figure The improvement in the jobless claims figure suggests to me that if the NFP do disappoint, investors are likely to blame it on the unusually bad weather. Nonetheless there could be a bigger-than-usual move in EUR/USD on a disappointing number because the usual sources of EUR supply – European market participants – will be out of the market for the Good Friday holiday. Remember how EUR/USD jumped during Fed Chair Janet Yellen’s press conference following the recent FOMC meeting, which took place after European markets had closed for the day. However, I would expect profit-taking and new short EUR/USD positions to be established rather quickly as many participants are likely to attribute any worse-than-expected result to the weather and assume that the April figures will resume showing an improvement. In any event, I would expect that the market is positioned for a weak number, so the pain trade – the big shock to the market – would be a higher-than-expected figure.

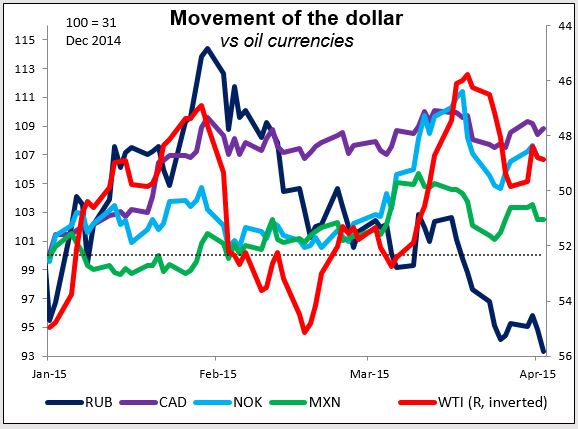

Brent plunges on Iran agreement Oil was down sharply, particularly Brent, after Iran and the world powers agreed on the main outlines of an accord that includes a timetable for lifting sanctions. Iran currently exports around 1mn b/d of oil but used to export 2.5mn b/d before sanctions began, meaning it could probably increase exports by over 1mn b/d. Of course the agreement is by no means a done deal; the two sides have until the end of June to work out the details, which probably will not be easy. Until then no additional Iranian oil will flow into the market. If they do reach agreement then, the additional Iranian oil would arrive just as the increased flow from North Dakota floods into a market where storage is filled up – a disaster-in-waiting.

CAD and NOK were relatively unaffected though as both gained vs USD. NOK seems to be the currency that is tracking oil prices most closely recently; I would expect it to weaken today as a result of the agreement.

China’s final HSBC services PMI for March was unchanged from the initial estimate of 51.8 even though the services sector PMI was revised up a bit. Nonetheless this shows the economy still expanding and lessens the need for further easing measures from the PBoC.

Today’s highlights: We have no major events or releases scheduled during the European session.

In the US, its nonfarm payrolls day! The March labor report will have a greater market significance than usual after Fed Chair Janet Yellen placed the importance of labor market strength over short-term inflationary expectations. Investors are likely to assume that a June rate hike could materialize if the next two NFPs come in strong. The market consensus is for an increase in payrolls of 245k, down from 295k in February. Even though the expected increase in March seems moderate compared to the astounding increases in the recent months, it would still be a strong figure consistent with a firming labor market. In the meantime, the unemployment rate is forecast to remain unchanged at 5.5%, while the average hourly earnings are expected to accelerate a bit on a mom basis. A robust labor report in line with estimates would keep the Fed on track to raise rates this year, which could boost confidence and strengthen USD.

As for the speakers, Minneapolis Fed President Narayana Kocherlakota and St. Louis Fed President James Bullard both give introductory remarks at two separate conferences. Kocherlakota is a major dove while Bullard is generally thought to be a centrist. It will be particularly useful to hear these two men’s views. If even they look for tightening this year, then it’s pretty much a foregone conclusion (although neither man votes on the FOMC this year).