- Sentiment recovers on signs that stimulus deal is still in play

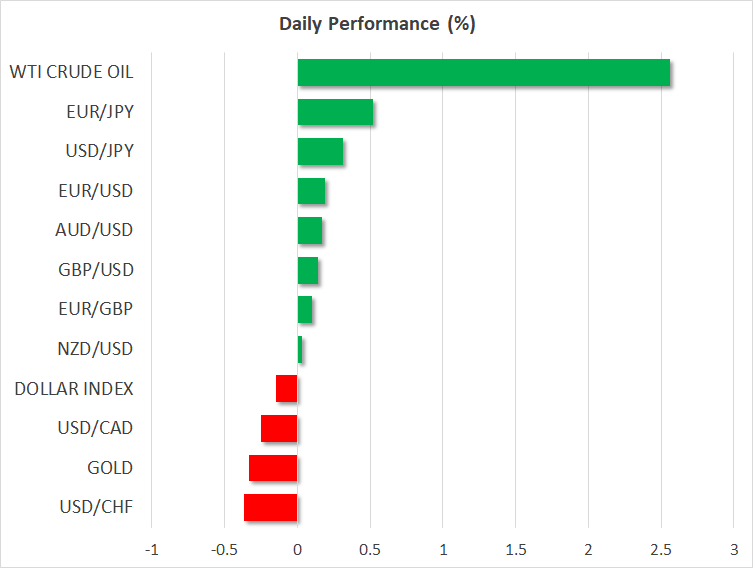

- Stocks rebound alongside crude oil, Japanese yen and gold retreat

- Markets to stay focused on ultimate game of ‘Deal or No Deal’

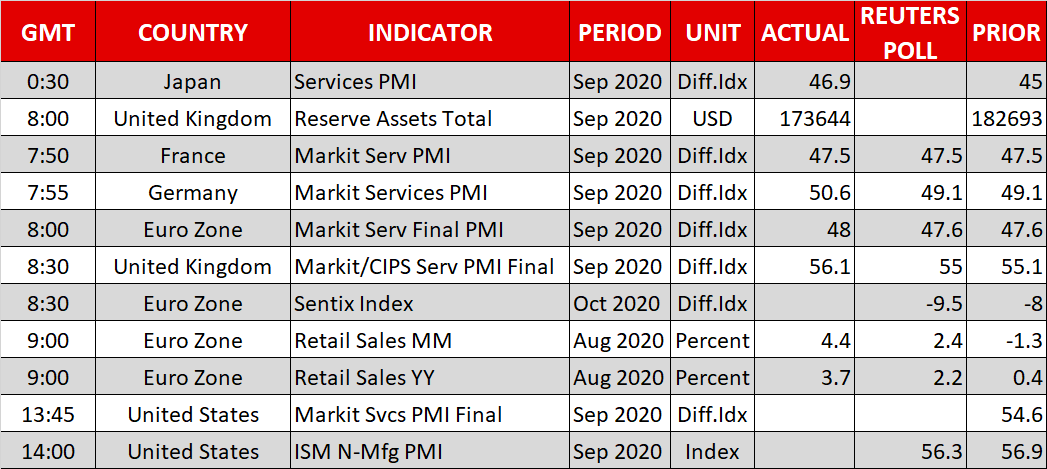

- Coming up: ISM non-manufacturing and RBA policy decision

Markets take solace from signs stimulus is coming

Global markets opened on a cheerful note on Monday, emboldened by hopes that a relief package deal can still be brokered in America and that President Trump’s health is improving. The news that Trump was diagnosed with coronavirus unleashed a wave of risk aversion late last week, driving global stocks lower and pushing investors into defensive assets, but nerves seem to have calmed down.

The sanguine mood likely comes down to a tweet by Trump that called on lawmakers to “work together” to get a stimulus deal done, fueling bets that the White House is prepared to concede some ground to strike an agreement. This was soon echoed by Senate Majority leader Mitch McConnell, who said “we are closer to getting an outcome”.

Trump’s sudden change of heart on this issue may be linked to the latest batch of opinion polls, which show that Biden increased his lead after last week’s hectic debate, reflecting what betting markets have been saying too. In essence, Trump is falling behind, so he needs to make something happen quickly if he is to turn the tide, and sending another round of checks to the public may just do the trick.

Reports that Trump may be discharged from the hospital today may be supporting sentiment as well. The Japanese yen and gold prices are back on the retreat, whereas crude oil is staging a comeback, drawing strength from futures contracts that point to a higher open on Wall Street today.

Deal is turning into a make-or-break event

Without many releases on the economic calendar this week, markets will stay laser-focused on the ultimate game of ‘Deal or No Deal’ that is being played on Capitol Hill. It is safe to say this has turned into a make-or-break event for many assets, as a lot of optimism for an eventual accord has already been baked into the cake.

The bottom line is that this market is now a hostage to incoming political headlines. While the tea leaves currently point to a deal being more likely than not, that could change in an instant and the time window for reaching an agreement is closing fast. The next ‘big move’ in stocks and the dollar will depend on whether the week ends with a deal or not.

Most other news is just a sideshow, something perfectly captured by the US employment report, which failed to spark any market reaction on Friday. Nonfarm payrolls clocked in at 661k, falling short of the 850k consensus. While the unemployment rate fell substantially, this was mostly thanks to a similar drop in the labor force participation rate, indicating that unemployment is falling mainly because discouraged workers are leaving the labor market altogether.

Brexit talks, ISM survey, and RBA meeting in focus

The dollar has been surprisingly quiet in recent sessions, staying trapped in a narrow range against the euro despite all the headlines. A stimulus deal would probably hurt the reserve currency both via the risk sentiment channel and via deficit worries. For now though, the dollar may take its cue from the ISM non-manufacturing PMI later today.

In politics, the Brexit talks will continue. The pound has been trading like a pinball machine lately and that is unlikely to change unless we see some progress on the final sticking points, which include fisheries and the level playing field.

Finally, the Reserve Bank of Australia will wrap up its meeting early on Tuesday, and if policymakers lay the groundwork for a rate cut in November, the aussie would be at risk.