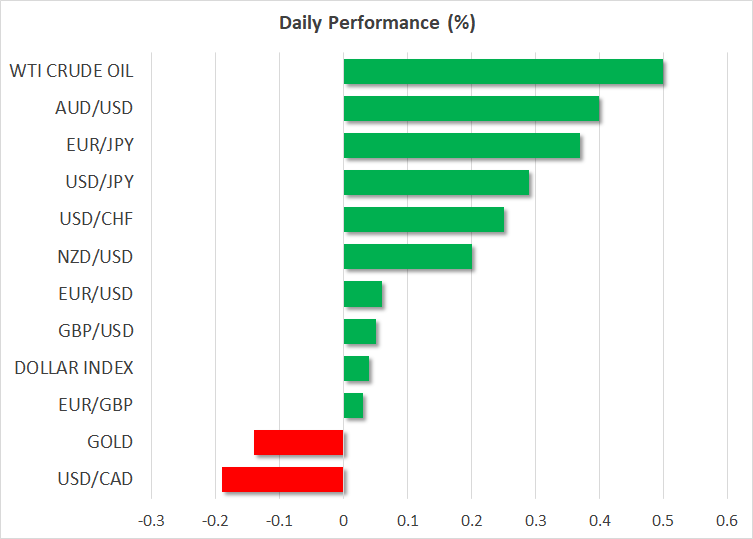

- Euro barely gains despite inflation overshoot and ECB talk

- Dollar stages late session comeback, stocks hover near records

- Crucial US data and OPEC+ meeting on the agenda today

Euro brushes positive news aside

The notion that the European Central Bank will slow down its asset purchases is gaining traction. Officials from Austria and the Netherlands threw their weight behind this yesterday, highlighting the positive economic surprises lately. That was soon echoed by ECB vice chief Luis de Guindos.

Their hawkish remarks were reinforced by an upside surprise in the Eurozone’s inflation rate, which jumped to 3% in August as supply chain disruptions continued to rage and summer demand kicked in. Another encouraging element is the elevated vaccination rate across Europe, which minimizes virus risks.

That said, all this talk about slashing asset purchases is mostly technical shenanigans, not a real taper. The ECB essentially has two QE programs in place right now, the crisis-era and the regular asset purchases. Policymakers want to slow their crisis-era interventions, but the total envelope of that program wouldn’t change. It was always fixed in size.

In other words, the ECB is about to tweak the speed, but not the total size of its crisis-fighting asset purchases. And there’s a strong chance that regular purchases are beefed up once that envelope is exhausted. Therefore, this wouldn’t be a real normalization of monetary policy, like the Fed is about to execute.

The Eurozone economy is doing better but there’s a risk this is mostly a reopening boom, as Germany’s disappointing retail sales suggested today. And the Recovery Fund is too small to make a real difference. Interest rate increases are not on the horizon, so the euro could struggle as the ECB is left behind in the central bank normalization race.

Dollar fights back, stocks hang on

In the broader market, it was a relatively quiet session as August came to a close. The dollar battled through some early adversity to close almost unchanged, drawing power from a rebound in US Treasury yields.

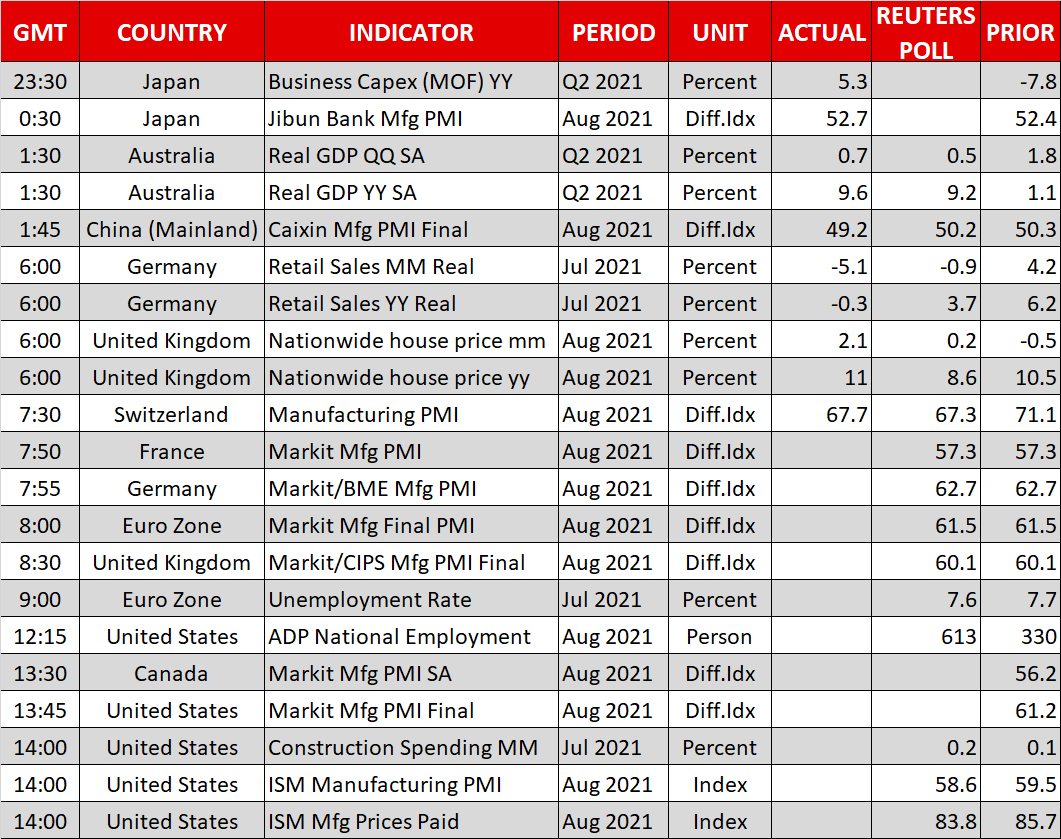

Markets are still grappling with when the Fed will push the taper button. The consensus seems to have settled around a November announcement, although that could be brought forward if Friday’s jobs report is sensational. We’ll get a taste of what to expect today when the ADP employment report and the ISM manufacturing PMI for August are released.

Meanwhile, Wall Street ended a volatile session marginally lower. The major indices remained just a shade away from record highs, as hopes for a super-slow Fed normalization and more fiscal juice from Congress eclipsed concerns that consumer spending may be cooling down. Indeed, the American consumer has gone on such a rampage this past year that some deceleration now is more than natural.

OPEC meeting in the spotlight

Beyond the US data releases today, markets will also keep a close eye on the OPEC+ meeting. The question is whether the cartel will stick to its plans to steadily raise production through the end of the year or whether the damage the Delta outbreak has inflicted on global demand will be enough to put those plans on ice.

It’s a close call, but ‘sources’ suggest OPEC and its allies will forge ahead with output increases. In this case, oil prices could come back under pressure as markets price in a less favorable supply/demand balance in the coming months. That could also hit the oil-sensitive Canadian dollar.

Of course, any negative reaction in both oil prices and the loonie may be relatively minor as this is the market’s baseline scenario already. The surprise would be if the producers shelved their plans to raise output, in which case the upside reaction in oil could be much bigger.