Greece comes down to the wire It looks like the talks between Greece and its creditors will come down to the wire. Germany yesterday rejected Greece’s request to extend its EUR 172bn rescue package by six months, but the Eurogroup of finance ministers will meet today to discuss it anyway. The stumbling block is apparently that Greece wants to find “mutually acceptable financial and administrative terms.” Germany argues that really, all Greece wants is a six-month bridging loan while they renegotiate the terms of the bailout. Germany (and several other countries) believe Greece should commit to fulfilling the same conditions that it agreed to under the previous administration, something that PM Tsipras has vowed not to do.

In fact, the FT said that Germany wants no more than a three-sentence letter from Greece requesting the extension, promising to complete its reform program and committing to negotiate any changes with bailout monitors. But the Greek government said it would not revise the letter and that the Eurogroup has just two choices: accept it or reject it. Rejecting it means, in effect, that Greece could go bust as early as next month, forcing it to either cut spending or default on debt payments. Greek banks would also lose some aid payments perhaps even emergency funding from the ECB, which could hasten the outflow of funds from the banking system. It is coming down to a game of chicken.

All is not lost yet, however. It’s notable that this meeting will be in person in Brussels, rather than by teleconference. Apparently that’s because of the need to forge a compromise. The meeting will be held at 1400 GMT. The finance ministers’ deputies met for seven hours yesterday and reportedly are “close to an agreement but subject to political discussion,” according to Market News. Also, it may be significant that this is a three-day weekend in Greece (and Cyprus as well). The same holiday was used in 2013 to impose the haircut on depositors in Cyprus’ banks.

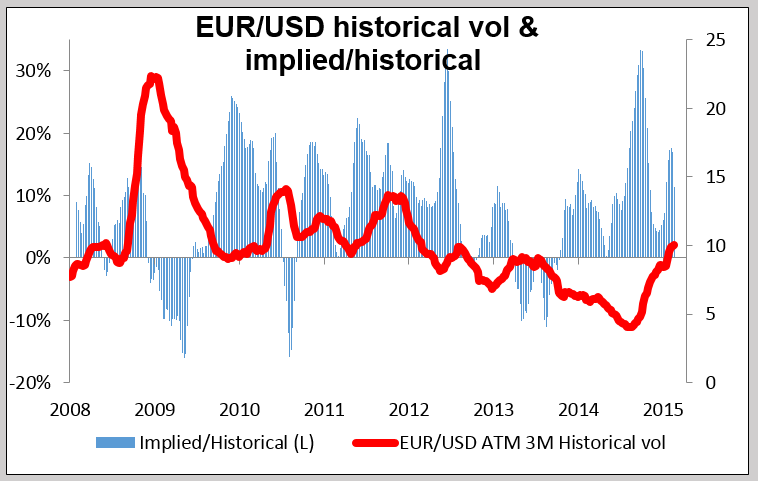

Even at this late date the FX market remains remarkably sanguine about the outcome of the talks. The EUR/USD risk reversal is almost exactly the same as the GBP/USD risk reversal, while implied vol on EUR/USD options is well within the normal range relative to historical. Greek stocks also ended the day up 1%, which although down from the midday level isn’t bad. Our simple average of three major Greek bank stocks rose 6.2% yesterday (vs +0.6% for the Eurostoxx banks index), which is also encouraging – apparently someone believes a successful conclusion is likely.

With the market already assuming a successful outcome, news of an agreement probably would not have that big an impact on EUR/USD. At best we might go back to the resistance line of 1.1450, in my view. The surprise would be a failure to come to an agreement. It’s not clear whether today’s deadline is really a deadline or just a very, very sick line, but in any event, failure to come to an agreement today would probably start people thinking more seriously about the consequences and raise the risk premium on EUR/USD, meaning it could head back to the lows of 1.1100.

US market thinking about Yellen’s testimony The leading index rose, but not by as much as it has been recently. Jobless claims continued to be volatile, which tells us more about problems with the seasonal adjustment than it does about the labor market. The Philadelphia Fed manufacturing survey was similar to the Empire State survey in that it too showed modest growth in manufacturing. So no change in the picture of continued steady but unspectacular growth in the US. The implied interest rates on Fed funds, which plunged in the wake of the dovish FOMC minutes on Wednesday, crept higher Thursday as investors re-read the minutes and thought about what Fed chair Janet Yellen is likely to say next Tuesday and Wednesday, when she gives her semi-annual testimony to Congress. She’s likely to be more in line with the hawkish comments that we’ve heard from other FOMC members recently, which could boost sentiment for the dollar.

Today’s highlights: Needless to say, the highlight of the day will be Greece once again.

As for the indicators, Friday is a PMI day. China is on holiday and so did not announce its PMI. Japan’s manufacturing PMI for February fell to 51.5 from 52.2, contrary to estimates. This was the lowest level since last July as new orders and employment slowed. The index is not particularly market-affecting for Japan, but the decline does make me think that once the election in April is past, the administration’s attention will return to producers rather than consumers and we are likely to see more willingness to talk down the yen.

During the European session, the preliminary manufacturing and service-sector PMI data from several European countries and the Eurozone as a whole are coming out. The manufacturing PMIs are expected to be higher, which could suggest that Eurozone economies have gained momentum in 2015 and could strengthen EUR, at least temporarily.

In the UK, retail sales for January are expected to fall, a turnaround from the previous month.

From Canada, we get the retail sales for December.

In the US, the preliminary Markit manufacturing PMI for February is coming out.

We have no speakers scheduled on Friday’s agenda.