Greece to dominate the day Today’s market will of course be dominated by developments in Greece. European finance ministers, including of course Greek FM Varoufakis, meet again in Brussels to hash out an agreement. Greek officials talked with the troika on Saturday and EU Commission President Juncker spoke to Greek PM Tsipras on Sunday, but there’s no news about what they decided, if anything. Anti-austerity rallies in support of SYRIZA were held in 20 cities around Europe over the weekend, increasing the pressure on EU politicians to compromise lest they get kicked out of office at the next election. I still expect that they will reach some agreement, although there is of course always some doubt. And even if they don’t, there are questions about when the real deadline is. As long as they’re in the euro, there is hope for some agreement. Nonetheless it was noticeable that the euro (and its shadow, the CHF) was the only G10 currency that isn’t opening higher against the dollar today than it was on Friday morning, despite the better-than-expected Q4 GDP figures announced on Friday. This suggests some measure of risk premium is creeping in. The Eurogroup meeting on Greece isn’t until the evening so I expect trading to be inconclusive until then and swayed by any headlines that emerge.

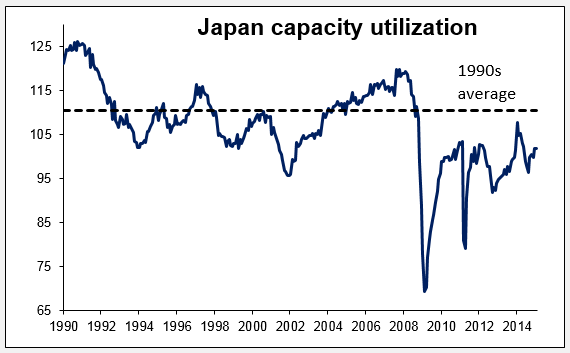

Japan’s growth disappoints Japan’s preliminary GDP for Q4 rose 2.2% qoq SAAR, a pretty weak result following two consecutive quarters of contraction and well below estimates of +3.7%. On a qoq basis, the rise was +0.6%, of which 0.2 ppt was a rise in inventories and another 0.2 ppts net exports, meaning that the domestic economy only contributed about one-third of the total demand growth – and this coming out of a recession. In the context of such weak growth, the markets will be listening closely to what BoJ Gov. Kuroda has to say on Wednesday following the BoJ meeting (see below). Capacity utilization is not yet back up even to the pre-financial crisis average, and the country was in deflation for 43% of that time. Clearly if he is expecting robust domestic growth to close the output gap and start pushing prices higher, he is going to wait a long time. Capacity utilization still isn’t back up to the level of the 1990sThat’s why I doubt that they are really so concerned about a weak yen and why I think they are likely to pursue that path further.

Today’s highlights: During the European day, the main event of the day will be the decisive Eurogroup meeting on Greek debt.

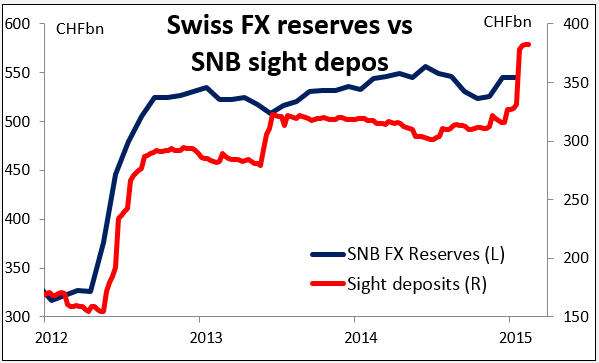

The Swiss National Bank releases its weekly sight deposit data, which could reveal if the Bank intervened in the FX market in the week ended Feb. 13. Indications of further intervention could weaken CHF somewhat.

Eurozone and Norway’s trade balance for December and January respectively are also coming out.

In the US, the markets are closed due to a national holiday (President’s Day).

We have only one speaker on Monday’s agenda: Riksbank Governor Stefan Ingves.

Rest of the week On Tuesday, the Reserve Bank Australia releases the minutes of its February meeting where it cut its benchmark interest rate by 25 bps. The minutes will probably show that the main reasons behind the rate cut are the low inflation and the rising unemployment. In Europe, the highlight will be the German ZEW survey for February. Both indices are forecast to have risen. This could be the 4th consecutive rise in the indices, adding further evidence to the surprisingly strong Q4 GDP that the German economy is gaining momentum. In the UK, CPI for January is expected to have eased further. This is likely to confirm the comments in Thursday’s inflation report that CPI may drop below zero in the coming months and remain close to zero for much of 2015. In Sweden, we get the CPIF – Riksbank’s favorite inflation gauge -- for January.

On Wednesday, the Bank of Japan holds a policy board meeting. The focus will be on Gov. Kuroda’s speech following the meeting and in particular, whether he comments on the news story that ran last week that BoJ policy makers believe further easing would be “counterproductive” as it could weaken the yen further and damage confidence. From the UK, we get unemployment rate for December and Bank of England February meeting minutes. The minutes may show a similar outlook with the Thursday’s inflation report that if deflation is more persistent than the forecast, the Bank is ready to cut interest rates if necessary or expand the Bank’s stimulus program. In the US, the Fed releases the meeting minutes of its Jan. 27-28 meeting. The statement was slightly more confident on the economy, with “solid job gains” upgraded to “strong job gains.” Any reference to when they may start normalization or even remove the line about being “patient” could boost USD. Wednesday also marks the start of the Lunar New Year in China and several other Asian countries.

On Thursday, the only noteworthy indicator we get is the usual US initial jobless claims.

Friday is PMI day. We get the preliminary Markit manufacturing and service sector PMIs for February from several European countries and the Eurozone as a whole, as well as manufacturing for the US. Also UK retail sales.