- Traders are biding their time as ECB and Fed decisions loom along with US CPI data

- White House infrastructure talks also in focus as negotiations drag on

- Stocks hover near highs as dollar ticks up, but US yields slip again

Dollar inches higher as ECB, Fed and inflation eyed

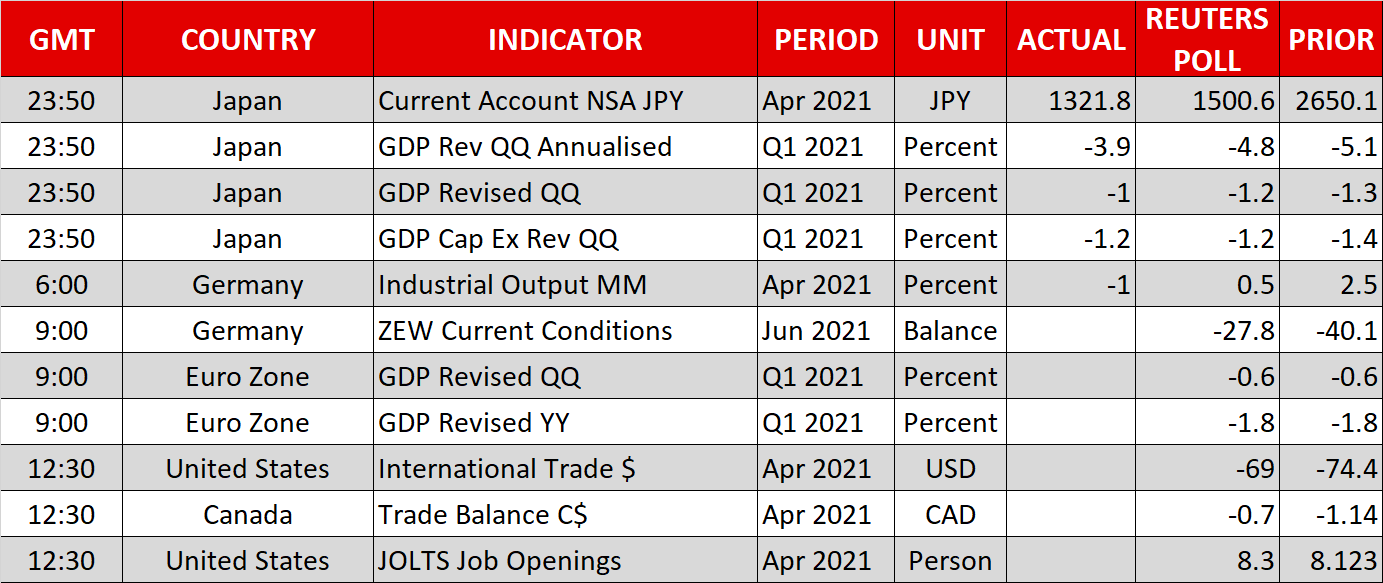

Markets were mostly drifting sideways on Tuesday, awaiting fresh clues on stimulus plans in Europe and the United States as fears of central bank tapering and higher inflation continue to haunt investors. The US consumer price index on Thursday will be one such clue and although a decision by the Fed to begin reducing its monthly bond purchases is still a few meetings away, the strength of the incoming data could determine whether tapering starts later this year or in early 2022.

Given that at most, the Fed is expected to telegraph the commencement of discussions when it meets next week, taper speculation will likely only intensify in the coming weeks.

However, the European Central Bank will probably try to avoid any mention of tapering on Thursday even though it is hard to imagine that policymakers haven’t begun to give any thought as to how the PEPP programme will be phased out. Nevertheless, the ECB’s coherently more dovish tone of late could put a dampener on the euro if it’s repeated on Thursday.

The single currency slipped slightly on Tuesday after failing to reclaim the $1.22 level on Monday. The dollar index, meanwhile, was up 0.2%, as the greenback advanced 0.3% against the yen and pound.

Stocks struggling for momentum

A broadly weaker yen underlined the slight risk-on mood as European stocks opened modestly higher, flirting with fresh record or recent highs. It follows a lacklustre session in Asia where many of the main indices were unable to hold onto earlier gains. US stock futures were also mixed, with the e-mini for the Nasdaq Composite last trading marginally in positive territory but S&P 500 and Dow Jones futures being slightly down.

The recent pullback in Treasury yields seems to be propping up Wall Street for now, particularly tech stocks, which are more sensitive to increases in long-term borrowing costs due to their sky-high valuations being determined by expectations of future earnings.

However, although both the S&P 500 and Dow Jones are on the cusp of closing at new all time-highs and the Nasdaq is extending its rebound from the May dip, there doesn’t seem to be much momentum in equity markets at the moment.

Still no deal on Biden’s infrastructure plan

One possible lift for stocks could come from a deal being reached between Congress and the White House for President Biden’s infrastructure proposal. The President has rejected the Republicans’ latest offer of just under $1 trillion as it still falls far short of the $1.7 trillion compromise he is seeking. Another round of talks is expected over the next day, after which, the Democrats may choose to go it alone.

However, that process could still lead to the infrastructure package being further watered down from the original $2.3 trillion, so it’s unclear how much of a boost any final deal would be for Wall Street.

In the meantime, as talks continue and ahead of the big day on Thursday, traders will be keeping an eye on the JOLTS job opening due later today out of the United States, as well as on the Treasury auction for $58 billion of three-year notes.